Five Charts to Start the Week

Some quick reminders before we get into it since there are more of you reading this now than there were last week. First, this is my diary on the market. It is in no way shape or form investment advice. These are the conversations that I am having with myself as I take in all that is happening in the market while trying to square it with the prevailing narratives and fundamentals. I do this to give some clarity to my thoughts. If you like what you are reading, please consider passing it along to others who might like it as well.

Next, if you have an opinion, I would love to hear it, especially if you disagree with something that I am thinking. I promise you that after starting in this business as a summer intern at the New York Stock Exchange when I was 16 years old, I have extremely thick skin.

Finally, nothing I write here should be considered investment advice. It is highly likely that I have a different timeframe and risk profile than you do.

Here are the five most interesting charts to me as the shortened week begins…

One of the biggest points that the bears like to make is that the market is “expensive.” They point to metrics like the P/E Ratio and the P/S ratio to make their point. Usually there is not much in the way context other than to site a number that is higher than a historical average and then tell people they are crazy for being bullish. But here is what they miss, valuation alone is not a catalyst. It is simply an environment. Is the market expensive by historical standards? Yes. Does that mean it has to go down right now? No. Take a look at Warren Buffett’s favorite metric for determining if the market is cheap or expensive, the ratio of US Stocks to GDP. This is a monthly chart with a 24-month moving average and bands set two standard deviations above and below the average. Notice how it broke out in October 1996 right before Fed Chairman Greenspan’s famous irrational exuberance speech in December of the same year. The market stayed “expensive” for more than three years after that breakout, and the speech, before the Internet bubble burst in March 2000.

Since the bears like to compare the current environment to 1999, I like to push back and say but what if this is only 1997? You can see that once again, the ratio has broken out (second dashed line) and is once again “expensive.” What if we have another three years of the market defying the valuation logic of the bears? More interesting is what happens if these bears ever capitulate…to me that would be the ultimate “sell signal.”

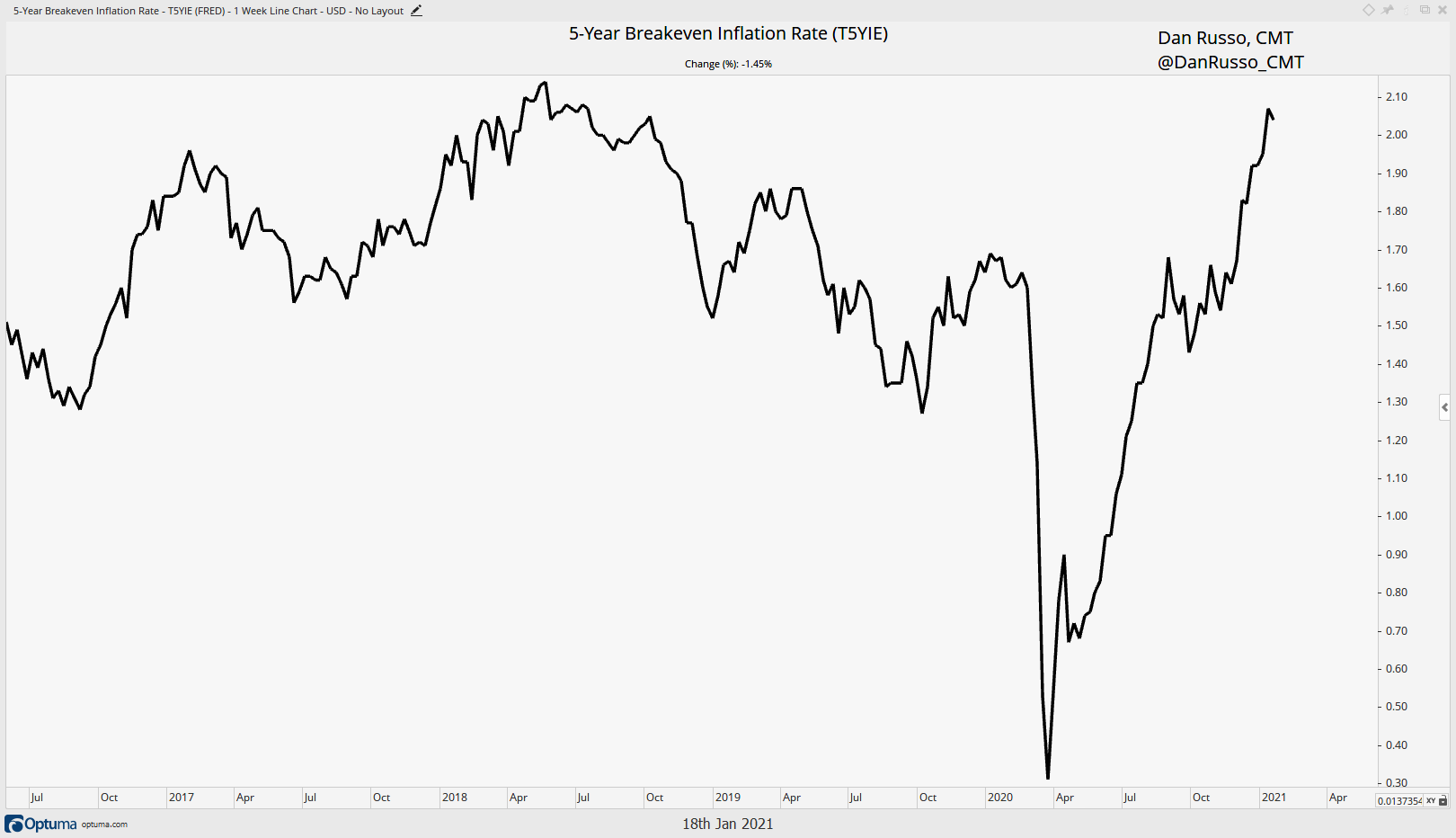

Next up is inflation. I have been on this theme for a while and some may be tired of hearing about it, but it really is a key driver to most of my views right now. Last week we heard that the Consumer Price Index (CPI) has higher on both a month over month and year over year basis…this is what happens when you can just print money. The Fed has told us that they are going to let inflation run hot before even thinking about thinking about raising rates. The market seems to agree. The five-year breakeven inflation rate is over the Fed’s target of 2%.

So, I think a higher level of inflation than we are used to should be the base case. With that in mind, I have spent a lot of time talking and writing about commodities. Here is something that I find really interesting though, many models that I have seen do not have an explicit allocation to this asset class. I could be wrong (and if someone with more experience with model portfolios wants to leave a comment, I would love to chat), but I just don’t see it. Maybe the fact that this asset class was in a 10 year downtrend has pushed many investors away? I think that we may actually get to a point in the next year or two where owning commodities over equities is the right strategic shift. I have been gradually increasing my exposure over the past few months. I think this has a lot of room to run and not many people appear to be positioned to ride this rising tide.

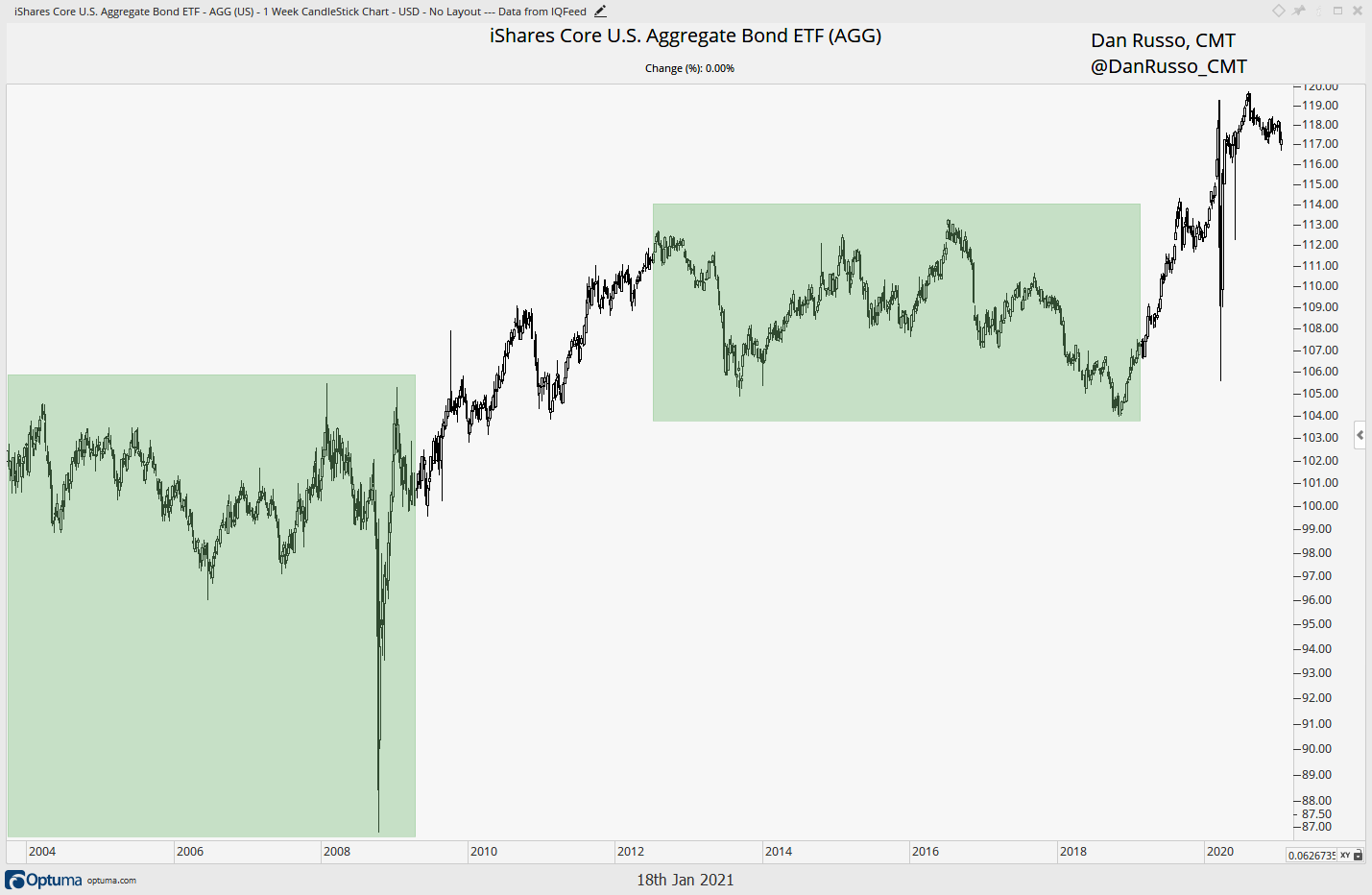

Perhaps even more amazing than the fact that many models / investors don’t have a meaningful allocation to commodities is that that they will normally maintain their exposures to fixed income. Yet from 2004 - 2009 and from 2012 - 2018 (green areas), a proxy for this asset class did nothing. I am of the mind that after a sharp rally from the 2018 lows into the COVID peak, there is scope for the iShares Core US Aggregate Bond ETF to do the same thinking again. This makes sense is there is inflation. Do you want to own an asset that pays a fixed coupon when the purchasing power of those coupons is being eroded by inflation and persistent money printing?

Aside from some real “banana republics” I am not sure if there is a more tainted region for investors than Europe. It has literally gone nowhere for 20 years. But now the region may be on the verge of a big breakout. This is interesting because when people think of investing abroad, they instinctively ( and correctly) think of Asia first. I know I do. It’s a better story from a growth perspective. I don’t have a good feel for what is driving this. Great Britain is a 23% weight so perhaps as the “brexit” drama nears an end, there is scope for a relief rally. The “scandies” held up better than the rest of the region through COVID but they are small. I should probably spend more time here.

Take-Aways:

Equity markets can probably stay “expensive” in light of an accommodative Federal Reserve because equities should be a good way to protect purchasing power in the event that inflation becomes an issue in the years ahead.

This should lead investors to commodities but thus far they seem to be under-owned but it appears that a new trend to the upside is beginning.

Owning bonds, which is the preferred portfolio diversifier may not work as well as purchasing power of coupon payments is impacted negatively.

I am not sure where a breakout in Europe fits into this theme but 20-year bases catch my attention so I included it here today.

Thank you for taking time out of your day to read to my thoughts. Please remember that nothing in these pages should be considered investment advice.